Contents

1. Introduction

The Local Government Pension Scheme (Management and Investment of Funds) Regulations 2016 require administering authorities to formulate and to publish a statement of its investment strategy, in accordance with guidance issued from time to time by the Secretary of State. The administering authority must invest, in accordance with its investment strategy, any Fund money that is not needed immediately to make payments from the Fund.

The regulations provide a new prudential framework, within which administering authorities are responsible for setting their policy on asset allocation, risk and diversity. The Investment Strategy Statement will therefore be an important governance tool for the Devon Fund as well as providing transparency in relation to how Fund investments are managed.

The Devon Pension Fund’s primary purpose is to provide pension benefits for its members. The Fund’s investments will be managed to achieve a return that will ensure the solvency of the Fund and provide for members’ benefits in a way that achieves long term cost efficiency and effectively manages risk. The Investment Strategy Statement therefore sets out a strategy that is designed to achieve an investment return consistent with the objectives and assumptions set out in the Fund’s Funding Strategy Statement.

We are long term investors: we implement our strategies through investments in productive assets that contribute to economic activity, such as equities, bonds and real assets. We diversify our investments between a variety of different types of assets in order to manage risk.

The Investment Strategy Statement will set out in more detail:

(a) The Devon Fund’s assessment of the suitability of particular types of investments, and the balance between asset classes.

(b) The Devon Fund’s approach to risk and how risks will be measured and managed, consistent with achieving the required investment return.

(c) The Devon Fund’s approach to pooling and its relationship with the Brunel Pension Partnership.

(d) The Devon Fund’s policy on how social, environmental or corporate governance considerations are taken into account in its investment strategy, including its stewardship responsibilities as a shareholder and asset owner.

Under the previous regulations the Fund was required to comment on how it complied with the Myners Principles. These were developed following a review of institutional investment by Lord Myners in 2000, and were updated following a review by the National Association of Pension Funds in 2008. While a statement on compliance with the Myners Principles is no longer required by regulation, the Devon Pension Fund considers the Myners Principles to be a standard for Pension Fund investment management. A statement on compliance is included at Annex 1.

This statement will be reviewed by the Investment and Pension Fund Committee at least triennially, or more frequently should any significant change occur.

Download or Print a copy of the 2025Investment Strategy Statement: Investment Strategy Statement June 2025.pdf

2. Investment Strategy and The Process for Ensuring Suitability of Investments

The primary objective of the Fund is to provide pension and lump sum benefits for members on their retirement and/or benefits on death before or after retirement for their dependants, in accordance with LGPS Regulations.

The Funding Strategy and Investment Strategy are intrinsically linked and together aim to deliver stable contribution rates for employers and a reduced reliance on employer contributions over time.

The investment objective is therefore to achieve sufficient return in excess of the actuarial discount rate, whilst minimising risk and the Fund’s exposure to a deep structural fall in markets which could potentially put pressure on the Fund and its employers. Having a thorough understanding of the risks facing the Fund is crucial and these are covered later in this statement. Additionally, the Fund is focused on increasing certainty of cost for employers and minimising the long-term cost of the Fund.

The Fund has the following investment beliefs which help to inform the investment strategy derived from the decision making process:

- Funding, investment strategy and contribution rates are linked.

- The strategic asset allocation is the key factor in determining the risk and return profile of the Fund’s investments.

- Investing over the long term provides opportunities to improve returns.

- Diversification across asset classes can help to mitigate against adverse market conditions and assist the Fund to produce a smoother return profile due to returns coming from a range of different sources.

- Managing risk is a multi-dimensional and complex task but the overriding principle is to avoid taking more risk than is necessary to achieve the Fund’s objectives.

- Environmental, Social and Governance are important factors for the sustainability of investment returns over the long term. More detail on this is provided below.

- Value for money from investments is important, not just absolute costs. Asset pooling is expected to help reduce costs over the long-term, whilst providing more choice of investments, and therefore be additive to Fund returns.

- Active management can add value to returns, albeit with higher short-term volatility.

- The Fund is keen to invest a maximum of 5% of its assets locally (defined as the Southwest region) subject to these investments meeting the broader financial objectives of the Fund.

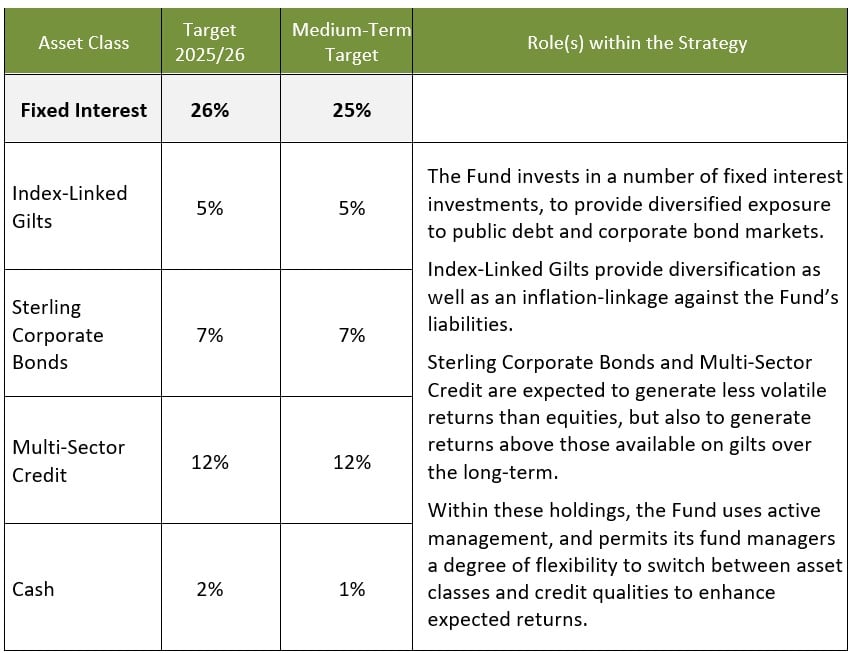

Current Investment Strategy

The Fund’s current investment strategy, along with an overview of the role each asset plays is set out in the table below:

Equities

Fixed Interest

Alternatives/Other

Full details of the current investment managers and their respective performance benchmarks are included in Annex 2.

Asset allocation varies over time through the impact of market movements and cash flows. The overall balance is monitored regularly, and if the allocations move more than 2.5% away from the target consideration is given to rebalancing the assets, taking into account market conditions and other relevant factors.

The Investment and Pension Fund Committee is responsible for the Fund’s asset allocation which is determined via strategy reviews undertaken as part of the valuation process. The last review of the investment strategy was in 2025 and was both qualitative and quantitative in nature, and was undertaken by the Committee in conjunction with officers and independent advisers. The review considered:

- The required level of return that will mean the Fund can meet its future benefit obligations as they fall due.

- An analysis of the order of magnitude of the various risks facing the Fund, incorporating both “Value-at-Risk” and historical stress test / hypothetical scenario analysis.

- The Fund’s current liquidity and cashflow position to ensure the Fund can meet its requirement to meet future benefit cash flows, both over the short-term and long-term.

- A range of climate / responsible investment analysis, including: climate scenarios, emissions and alignment-based metrics, and the proportion of the Fund’s investments generating positive impact.

- The desire to increase the proportion of the Fund invested locally, provided these investments meet the Fund’s broader financial objectives.

- The desire for diversification across asset class, region, sector, and type of security.

The investment consultants which the Fund procured to undertake this review, Redington, brought together the above considerations into a Pension Risk Management Framework (“PRMF”) to help the Committee assess the value of the options put forward for revisions to the Fund’s investment strategy.

Following the latest investment strategy review, the Committee agreed to a number of revisions to the investment strategy. These changes include reducing the allocation to listed equity and increasing the allocation to fixed income and private market investments, via allocations to index-linked gilts and nature-based solutions. Given the strong funding position the Fund has achieved, the changes introduced reduce risk and increase income generation whilst marginally reducing expected returns. Additionally, given the Fund’s focus on responsible and local investment, the addition of Natural Capital and increasing the allocation to the Local Impact Portfolio will add diversification whilst helping to meet the Fund’s Environmental Social and Governance (ESG) objectives.

Details of the 2025/26 target allocations and the agreed medium-term plan are shown in the table above. It should be noted that progress in reaching the targets will be dependent upon a number of factors, including market movements, the progress of the Fund’s pooling partner in identifying suitable private market commitments and the pace of the subsequent draw down of commitments.

The medium-term plan will be regularly reviewed by the Committee in conjunction with officers of the Fund and it’s Independent Investment Advisor.

In accordance with the requirements of the LGPS (Management and Investment of Funds) Regulations 2016, the Investment Strategy will not permit more than 5% of the total value of all investments of fund money to be invested in entities which are connected with the Authority within the meaning given by applicable legislation.

3. Risk Measurement and Management

Successful investment involves taking considered risks, acknowledging that the returns achieved will to a large extent reflect the risks taken. There are short-term risks of loss arising from default by brokers, banks or custodians but the Fund is careful only to deal with reputable counter-parties to minimise any such risk.

Longer-term investment risk includes the absolute risk of reduction in the value of assets through negative returns (which cannot be totally avoided if all major markets fall). It also includes the risk of under-performing the Fund’s performance benchmark (relative risk).

Different types of investment have different risk characteristics and have historically yielded different rewards (returns). Equities (company shares) have produced better long-term returns than fixed interest bonds but they are more volatile and have at times produced negative returns for long periods.

In addition to targeting an acceptable overall level of investment risk (one which is minimised to the extent possible whilst maintaining sufficient expected returns) the Committee seeks to spread risks across a range of different sources, believing that diversification limits the impact of any single risk. The Committee aims to take on those risks for which a reward, in the form of excess returns, is expected over time.

The key investment risks that the Fund is exposed to are:

- The risk that the Fund’s growth assets in particular do not generate the returns expected as part of the funding plan in absolute terms.

- The risk that the Fund’s assets do not generate the returns above inflation assumed in the funding plan, i.e. that pay and price inflation are significantly more than anticipated and assets do not keep up.

- That there are insufficient funds to meet liabilities as they fall due.

- That active managers underperform their performance objectives.

The Fund may be adversely impacted by a combination of the risks set out above over a given timeframe. While it is understood that over the long term, downside events are expected to be more than offset by a subsequent recovery and further asset growth, it is important for the Fund to closely monitor the risk exposure of its investment strategy.

As part of the latest investment strategy review, the Committee defined a risk budget for the Fund’s investment strategy of 15%, expressed in terms of asset Value-at-Risk (VaR) 95%. VaR is a common measure of risk which looks at the minimum fall expected in asset value in a 1-in-20 downside scenario. The Fund’s existing strategy had an asset VaR 95% of 15.1% (representing a c.£928m fall in the value of the Fund’s assets)1 and the revisions to the investment strategy the Committee approved brought this measure in line with the set risk budget. This risk budget is captured in an objective in the Fund’s PRMF alongside objectives for return, liquidity/cashflow and responsible and local investment. VaR is not a perfect risk measure and can understate risk in extreme scenarios, so the risk assessment was complemented with additional stress and scenario tests in the strategy review to ensure robustness of the Fund’s investment strategy under a variety of conditions.

At Fund level, these risks the Fund is exposed to are managed through:

- Diversification of investments by individual holding, asset class and by the investment managers appointed on behalf of the Fund by the Fund’s pooling partner.

- Robust oversight of the Fund’s primary investment manager, LGPS investment pool.

- Consideration of climate related risk in setting investment strategy and selecting investments for the Fund.

- Allocating to inflation-aware and cashflow generative investments within the asset portfolio.

- Ongoing monitoring of the Fund’s short, medium and long term cashflows to ensure sufficient liquidity to meet pension payments as they fall due.

- Explicit mandates governing the activity of investment managers.

- The appointment of an Independent Investment Advisor.

The external investment managers can control relative risk to a large extent by using statistical techniques to forecast how volatile their performance is likely to be compared to the benchmark. The Fund can monitor this risk and impose limits.

The Fund is also exposed to operational risk; this is mitigated through:

- A strong employer covenant.

- The use of a Global Custodian for custody of assets.

- Having formal contractual arrangements with investment managers.

- Comprehensive risk disclosures within the Annual Statement of Accounts.

- Internal and external audit arrangements.

The ultimate risk is that the Fund’s assets produce worse returns than assumed by the Actuary, who values the assets and liabilities every three years, and that as a result, the solvency of the Fund deteriorates. To guard against this the Investment Principles seek to control risk but not to eliminate it. It is quite possible to take too little risk and thereby to fail to achieve the required performance. Ongoing monitoring of the Fund’s investment strategy against the objectives set in the PRMF will assist with assessing the appropriate levels on investment risk and return on an ongoing basis, alongside broader objectives.

The Fund also recognises the following (predominantly non-investment) risks:

Longevity risk: this is the risk that the members of the Fund live longer than expected under the Actuarial Valuation assumptions. This risk is captured within the Actuarial Valuation report which is conducted at least triennially and monitored by the Committee, but any increase in longevity will only be realised over the long term.

Sponsor Covenant risk: the financial capacity and willingness of the sponsoring employers to support the Fund is a key consideration of the Committee and is reviewed on a regular basis.

Liquidity risk: the Committee recognises that there is liquidity risk in holding assets that are not readily marketable and realisable. Given the long-term investment horizon, the Committee believes that a degree of liquidity risk is acceptable, given the potential return. The majority of the Fund’s assets are realisable at short notice.

Regulatory and political risk: across all of the Fund’s investments, there is the potential for adverse regulatory or political change. Regulatory risk arises from investing in a market environment where the regulatory regime may change. This may be compounded by political risk in those environments subject to unstable regimes. The Committee will attempt to invest in a manner which seeks to minimise the impact of any such regulatory or political change should such a change occur.

Exchange rate risk: this risk arises from unhedged investment overseas. The Fund has a currency hedging policy in place, hedging up to 100% of its exposure to currency risk on passive equity holdings. For other asset classes, currency hedging is reviewed on a case-by-case basis.

Climate Change risk: climate change is a systemic investment risk that may have an impact on investee companies as a result of both the consequences of climate change and the transition to a low carbon economy.

As part of the 2025 investment strategy review, the Fund requested Redington carry out climate scenario analysis to estimate the impact of future warming scenarios on its asset portfolio. Redington uses 3 climate scenarios from the Network for Greening the Financial System (“NGFS”) as below:

- 2°C Disorderly Transition : this is illustrative of a scenario where rapid and unexpected policy changes occur in a panicked effort to limit global warming to 2°C. This scenario represents the highest level of transition risk.

- 2°C Orderly Transition: this is the lowest-risk scenario, and is illustrative of countries gradually increasing the stringency of climate policies to increase the likelihood of global warming being limited to 2°C.

- Hot House World: this is illustrative of a global warming scenario where a climate tipping point could be reached and warming is worse than expected. This scenario accounts for countries’ national climate policy pledges (even if they have not yet been implemented) and 5°C of warming.

The 2°C Disorderly and Hot House World scenarios showed the worst combined risk for the Fund’s asset portfolio. Transition risk is the most material risk under the 2°C Disorderly scenario, whereas physical risk is the most significant under the Hot House World Scenario.

The Fund’s approach to climate change is included in section 5 of the Investment Strategy Statement, and the Fund will expect it’s pooling partner and other fund managers to have policies in place to manage the risk. As part of the 2025 investment strategy review, the Committee approved a 3% allocation to natural capital which will support the Fund in meeting its climate objectives.

Cashflow risk: the Fund is marginally cashflow negative, in that income and disinvestments are required from the Fund’s investments to meet benefit outgoes. Over time, it is expected that the size of pensioner cashflows will increase as the Fund matures and greater consideration will need to be given to raising capital to meet outgoings. The Committee recognises that this can present additional risks, particularly if there is a requirement to sell assets at inopportune times, and so looks to mitigate this by investing in cashflow generative assets and by taking income from investments where possible.

Governance: members of the Committee and Devon Pension Board participate in regular training delivered through a formal programme. Both the Committee and Devon Pension Board are aware that poor governance and in particular high turnover of members may prove detrimental to the investment strategy, fund administration, liability management and corporate governance and seeks to minimise turnover where possible.

4. Approach to Asset Pooling

The Devon Pension Fund participates with nine other Administering Authorities to pool investment assets through the Brunel Pension Partnership Ltd. At the centre of the partnership is Brunel Pension Partnership Limited (Brunel), a company established specifically to manage the assets within the pool.

The Devon Pension Fund, through the Investment and Pension Fund Committee, retains the responsibility for setting the detailed Strategic Asset Allocation for the Fund and allocating investment assets to the portfolios provided by Brunel.

The Brunel Pension Partnership Ltd, established in July 2017, is a company wholly owned by the Administering Authorities (in equal shares) that participate in the pool. The company is authorised by the Financial Conduct Authority (FCA). It is responsible for implementing the detailed Strategic Asset Allocations of the participating funds by investing Funds’ assets within defined outcome focused investment portfolios. In particular, it researches and selects the external managers or pooled funds needed to meet the investment objective of each portfolio. Brunel will create collective investment vehicles for quoted assets such as equities and bonds; for private market investments it will create and manage an investment programme with a defined investment cycle for each asset class.

As a client of Brunel, the Devon Pension Fund has the right to expect certain standards and quality of service. The Service Agreement between Brunel and its clients sets out in detail the duties and responsibilities of Brunel, and the rights of the Devon Fund as a client. It includes a duty of care of Brunel to act in its clients’ interests.

The governance arrangements for the pool have been established. The Brunel Oversight Board is comprised of representatives from each of the Administering Authorities and two fund member observers, with an agreed constitution and terms of reference. Acting for the Administering Authorities, it has ultimate responsibility for ensuring that Brunel delivers the services required to achieve investment pooling and deliver each Fund’s investment strategy. Therefore, it has a monitoring and oversight function. Subject to its terms of reference it will consider relevant matters on behalf of the Administering Authorities but does not have delegated powers to take decisions requiring shareholder approval. These will be remitted back to each Administering Authority individually. As shareholders of Brunel, the Administering Authorities’ shareholder rights are set out in the Shareholders Agreement and other constitutional documents.

The Oversight Board will be supported by the Client Group, comprised primarily of pension investment officers drawn from each of the Administering Authorities but will also draw on Administering Authorities finance and legal officers from time to time. It has a primary role in reviewing the implementation of pooling by Brunel, including the plan for transitioning assets to the portfolios. It provides a forum for discussing technical and practical matters, confirming priorities, and resolving differences. It is responsible for providing practical support to enable the Oversight Board to fulfil its monitoring and oversight function. The Client Group will monitor Brunel’s performance and service delivery for each of the established Brunel portfolios. The Devon Investment and Pension Fund Committee will receive regular reports covering portfolio and Fund performance and Brunel’s service delivery.

The proposed arrangements for asset pooling for the Brunel pool were formulated to meet the requirements of the Local Government Pension Scheme (Management and Investment of Funds) Regulations 2016 and Government guidance. Regular reports have been made to Government on progress, and the Minister for Local Government has confirmed on a number of occasions that the pool should proceed as set out in the proposals made.

Devon County Council approved the full business case for the Brunel Pension Partnership in 2017. The process of transitioning the Fund’s assets to portfolios managed by Brunel started in April 2018, and was largely completed during 2021.

It is intended that all of the Devon Pension Fund’s assets will be invested through Brunel portfolios. However, the Fund has certain commitments to long term illiquid investment funds which will take longer to transition across to the Brunel portfolios. These assets will be managed in partnership with Brunel until such time as they are liquidated, and capital is returned.

5. Social, Environmental and Corporate Governance Policy

Overarching Principles

The Devon Pension Fund has a fiduciary duty to seek to obtain the best financial return that it can for its members. This is a fundamental principle, and all other considerations are secondary. However, the Devon Pension Fund is also mindful of its responsibilities as a long term shareholder, and the Investment and Pension Fund Committee has considered the extent to which it wishes to take into account social, environmental or ethical issues in its investment policies. The Devon Pension Fund’s policy is to prioritise engagement with companies to effect change.

In the light of that overarching approach the following principles have been adopted:-

- The Devon Pension Fund seeks to be a long term responsible investor. The Fund believes that in the long term it will generate better financial returns by investing in companies and assets that demonstrate they contribute to the long term sustainable success of the global economy and society.

- Social, environmental and ethical concerns will not inhibit the delivery of the Devon Fund’s investment strategy and will not impose any restrictions on the type, nature of companies/assets held within the portfolios that the Devon Fund invests in. However, the identification and management of ESG risks that may be financially material is consistent with our fiduciary duty to members.

- The Devon Pension Fund will seek to engage (through the Brunel Pension Partnership, its asset managers or other resources) with companies to ensure they can deliver sustainable financial returns over the long-term as part of comprehensive risk analysis. In the example of fossil fuels, this will mean engaging with oil companies on how they are assessing and diversifying their business strategy and capital expenditure plans to adapt to changes in cost base and regulation that will ensure the continued delivery of shareholder returns in the medium to long term. Engagement with companies is more likely to be successful if the Fund continues to be a shareholder.

- Where social, environmental and ethical issues arise on the agendas of company Annual General Meetings, the Brunel Pension Partnership, and its external investment managers are expected to vote in alignment with the Fund’s interest on investment grounds. Some issues may be incorporated into generally accepted Corporate Governance Best Practice (e.g. the inclusion of an Environmental Statement in the Annual Report and Accounts). In this case the Council will instruct its external investment managers to vote against the adoption of the Annual Report, if no such statement is included.

- The Devon Pension Fund recognises the risks associated with environmental, social and governance (ESG) issues, and the potential impact on the financial returns if those risks are not managed effectively. The Fund therefore expects its external fund managers to monitor and manage the associated risks. The Devon Pension Fund will work with its partners in the Brunel pool and the Brunel Pension Partnership Limited company to ensure that robust systems are in place for monitoring ESG risk, both at a portfolio and a total fund level, and that the associated risks are effectively managed.

- More broadly the Fund adopts the policies set out in the Brunel Responsible Investment Policy. The Brunel policy can be found at: https://www.brunelpensionpartnership.org/responsible-investment/responsible-investment-policy/

Climate Change

The Devon Pension Fund believes climate change poses significant risks to global financial stability and could thereby create climate-related financial risks to the Fund’s investments unless action is taken to mitigate these risks. In recognising the need to address the risks associated with climate change posed to both the Fund’s investments and our beneficiaries, we acknowledge that there is an urgent need to accelerate the transition towards global net zero emissions and play our part in helping deliver the goals of the Paris Agreement.

The Devon Pension Fund also believes investing for a positive climate scenario presents an opportunity to improve asset returns by harvesting a low carbon transition premium. This positive impact is expected to be most material over the period ending 2030.

The Devon Pension Fund has therefore pledged that its portfolio of investments will be net-zero by 2050 at the latest. In order to achieve this goal, the Fund has set the following targets:

- A 7% per annum reduction in the Weighted Average Carbon Intensity (WACI) of the Fund’s investments, based on the March 2019 calculation of the WACI. This recognises the need for significant progress in the earlier part of the period to 2050, with the intention of achieving a 50-75% reduction by 2030.

- These targets will also be applied to the Fund’s exposure to fossil fuel reserves as a proxy for downstream scope 3 emissions which are not captured within the WACI calculation.

- Within the Fund’s infrastructure investments, we would expect a significant proportion to be invested in renewable energy assets. The target is to achieve an allocation of 5% of the total Fund to renewable energy infrastructure assets by 2025.

- Alignment to the Paris Agreement – The target is that 100% of developed listed equities should be aligned or aligning by 2030 and 100% of all listed equities should be aligned or aligning by 2040. For a company to be considered to be aligned they need to:

- Have credible targets to achieve net zero and strategy to deliver them

- Engage positively to achieve those targets (including not lobbying against climate change mitigation, directly or via affiliations)

- Align financial processes and accounts

- Publicly disclose on the above.

- Engagement – Implement an engagement goal to ensure 70% of financed emissions in material sectors for listed equity and corporate bonds are either Net Zero, aligned to Net Zero pathways, or subject to direct or collected engagement and stewardship actions by June 2024, and that the threshold should be 90% by June 2027.

- Devon County Council has committed to reduce the carbon emissions from its operations to net-zero by 2030. This will include the operational emissions of the Devon County Council Investment Team in the oversight of the Fund’s investments, and the administration of benefits by Peninsula Pensions.

This will be achieved by the following strategy:

- We recognise that climate change will have impacts across our portfolios. This means we look to the Brunel Pension Partnership and all our asset managers to identify and manage climate-related financial risks as part of day-to-day fund management. The way those risks and opportunities present themselves varies, particularly in evaluating what a portfolio aligned to the Paris Agreement looks like.

- The Devon Pension Fund wants to play its part in achieving real economy emissions reductions. This means that we are looking for investee companies to make significant reductions in their emissions, rather than just shifting our investments from higher emitting companies to lower emitting companies. The Fund therefore prioritises engagement over divestment, particularly for listed equities. By integrating climate change into risk management process, using carbon footprinting, assessing fossil fuel exposure and challenging managers on physical risks, we seek to both reduce climate and carbon risk and achieve real reductions in global emissions. Where investee companies fail to engage with climate change issues, selective divestment may be appropriate based on inability or unwillingness to align to objectives of Paris Agreement, consistent with managing investment risk.

- We are committed to working with Brunel to decarbonise our investments in listed portfolios. Decarbonisation is achieved by being selective in the allocation of capital, particularly to carbon intense companies. This process is informed by using a variety of tools in combination with industry and corporate engagement. For example, engagement with electric utility companies about their future strategy on energy sources informs the investment decisions relating to those companies and indeed the relative attractiveness of the sector over time.

- We are committed to working with Brunel to decarbonise our investments in listed portfolios. Decarbonisation is achieved by being selective in the allocation of capital, particularly to carbon intense companies. This process is informed by using a variety of tools in combination with industry and corporate engagement. For example, engagement with electric utility companies about their future strategy on energy sources informs the investment decisions relating to those companies and indeed the relative attractiveness of the sector over time.

- We expect the engagement and voting conducted on behalf of the Fund by LAPFF, Brunel and underlying investment managers to be consistent with an objective for all assets in the portfolio to achieve net zero emissions by 2050 or sooner. The Fund’s stewardship and voting policies are set out more fully below.

- Climate change risk and carbon reduction targets will be a consideration in reviews of the Fund’s strategic asset allocation. This will be considered ensuring consistency with the Fund’s fiduciary duty to achieve the investment returns required to meet its future pension liabilities.

- The Devon Pension Fund adopts the Brunel Pension Partnership’s climate change policy, found at the following link:

https://www.brunelpensionpartnership.org/climate-change/ - The Devon Pension Fund views the Brunel policy as being representative of the climate change objectives of the Fund and in support of the wider objectives of Devon County Council.

- We are committed to being transparent about the carbon intensity of our investments through the publication of the Fund’s carbon footprint and reserves exposure on an annual basis through the Pension Fund Annual Report. This will enable us to measure progress against the targets set out above. The Fund will also report on delivery through the Brunel Annual Climate Action Plan and report in line with anticipated LGPS Regulation requirements in the 2023/24 Annual Report.

Accountability

The Pension Board regularly reviews all the Fund’s statutory statements. Their views will be taken into account in setting the Devon Pension Fund’s environmental, social and governance policies. The Fund also holds an annual consultative meeting with fund members which provides the opportunity for discussion of investment strategy and consideration of non-financial factors.

6. Stewardship Policy

The Devon Pension Fund is committed to responsible stewardship and believe that through stewardship it can contribute to the care, and ultimately long-term success, of all the assets within our remit.

The Fund supports and applies the UK Stewardship Code 2020 definition of stewardship: “Stewardship is the responsible allocation, management, and oversight of capital to create long-term value for clients and beneficiaries leading to sustainable benefits for the economy, the environment and society.”

The Devon Pension Fund works with or through the Brunel Pension Partnership, the Local Authority Pension Fund Forum and/or other partners to pursue activities which are outcomes focused, which prioritise the pursuit and achievement of positive real-world goals, and where there is enhanced collaboration which focuses on collective goals to address systemic issues. From a bottom up perspective, this includes:

- Engaging with companies and holding them to account on material issues.

- Exercising rights and responsibilities, such as voting.

- Integrating environmental, social and governance factors into investment decision making.

- Monitoring assets and service providers.

- Collaborating with others.

- Advancing policy through advocacy.

The Devon Pension Fund fully endorses and supports the Brunel Pension Partnership Stewardship Policy, and the Devon Pension Fund policy should be seen as fully consistent in all aspects.

The following section sets out in detail the Fund’s policies on stewardship, including its policy on the exercise of rights, including voting rights, attached to investments:

(a) Governance and Oversight

The Investment and Pension Fund Committee approves and is collectively accountable for the Devon Pension Fund’s policies, which includes the Stewardship Policy. Operational accountability on a day-to-day basis is held by the Head of Investments at Devon County Council, who is supported by the Investment Manager to ensure high levels of coordination and implementation. The Devon Pension Fund requires the Brunel Pension Partnership to provide a suite of public reports on their stewardship activities, and environmental, social and governance metrics to empower the Devon Pension Fund’s stewardship activities and to enable oversight.

The Fund believes in the importance of regular and in-depth shareholder and stakeholder engagement. Our Stewardship Policy has been developed in conjunction with that of the Brunel Pension Partnership, which in turn has been developed in collaboration with key stakeholders, including the Brunel Oversight Board, Brunel Client Group, and the Client Responsible Investment (RI) Sub-Group. The RI Sub-Group is made up of members of Brunel’s clients and meets monthly, it provides an opportunity for clients to:

- Raise stewardship interests.

- Share best practice with Brunel and amongst partner funds.

- Provide insights on concerns, issues, and member perspectives.

- Shape priorities of Brunel and Equity Ownership Services (EOS) at Federated Hermes.

- Review reporting outputs.

- Knowledge share and receive a deeper dive into topics of interest.

- Access expertise.

- Consult on policy design and development.

(b) Identifying and Prioritising Engagement

The Devon Pension Fund will expect Brunel to identify engagement objectives in four ways.

- Firstly, top down, to identify thematic areas of risk and opportunity.

- Secondly, bottom up, to review exposure to individual companies and to specific ESG risks and opportunities. Companies should be identified through asset managers, collaborative engagement forums, external research, and Brunel’s own internal ESG risk analysis.

- Thirdly, reactively to events, for example, after a specific, usually significant, incident. The companies that Brunel actively engage with should be prioritised based on our level of exposure and the probability of successful outcome.

- Fourthly, Brunel should be responsive to client concerns. Where the Devon Pension Fund raises specific issues, which could be as a result of Fund member concerns or points raised by Investment and Pension Fund Committee or Pension Board members, Brunel will be expected to engage with companies to address the concerns raised.

The Devon Pension Fund is a global investor and seeks to apply the principles of good stewardship globally. It is a strong advocate of the benefits of global stewardship codes to improve the quality of stewardship, and when updates are made aims to adopt best practice. As a UK-based investor our key reference points are the UK Stewardship Code 2020 and UK Corporate Governance Code and guidance produced by UK industry bodies, for example, the British Venture Capital Association (BVCA – private equity) RI toolkit.

The Fund is committed to supporting policy makers, regulators and industry bodies in the development and promotion of the codes and supporting guidance. The Fund publishes an annual review of its stewardship and engagement activities in its Annual Report which is intended to meet the best practice requirements of the UK Stewardship Code 2020 and support the Fund’s compliance with the Shareholder Rights Directive II. The Fund is a strong supporter of the UK Corporate Governance Code and the application of the Companies Act S172 (Duty to promote the success of the company). It believes that corporate behaviour in line with the spirit of the Act more broadly is essential to the Fund’s objective of contributing to a more sustainable and resilient financial system, which supports sustainable economic growth and a thriving society.

The Fund encourages companies either to comply with such codes or to fully explain their reasons for noncompliance. However, it is also cognisant that good governance cannot be guaranteed solely by adherence to the provisions of best practice governance codes. Therefore, we urge companies to consider carefully how best to apply the principles and the spirit of such codes to their own circumstances and to clearly communicate to investors the rationale behind their chosen approach.

(c) Transparency and Collaboration

Good stewardship requires a good understanding of the assets that the Devon Pension Fund invests in. This is done in collaboration with Brunel, who do it directly, through EOS at Federated Hermes, their asset managers, and other initiatives. Working closely with company boards is one of the most effective means to achieve this but requires the establishment of mutual trust and, at times, confidentiality. It is also acknowledged that, when working collaboratively with other investors, we must respect other disclosure requirements and restrictions.

The Fund publishes regular updates on its stewardship activities, including quarterly engagement and voting activity analysis presented to the Investment and Pension Fund Committee, and the annual review included in the Fund’s Annual Report.

The Fund believes that working collaboratively is essential to delivering its objectives as the scope and scale of investments means that we need to draw on the expertise of others, including Brunel, the Local Authority Pension Fund Forum (LAPFF), and not least the asset managers employed by both Brunel and directly by the Fund. In addition to managers and specialist advisors, the Fund supports a number of organisations and initiatives that enable its ability to work collaboratively – for example this includes membership of LAPFF and the Institutional Investors Group on Climate Change (IIGCC). The Fund’s reporting will evidence its activities.

(d) Conflicts of Interest

Devon County Council has a robust Code of Conduct and Conflicts of Interest policy, which all members of the Investment and Pension Fund Committee (whether Devon County Councillors or not) are required to adhere to.

Investment and Pension Fund Committee members are required to make declarations of interest prior to committee meetings in line with the Council’s code of conduct and interest rules. This would ensure that if committee members had any personal interests in any company that the Fund invests in that may have an impact on stewardship activity then those interests would be declared and managed.

The management of conflicts is important in building long-term relationships with the companies the Devon Pension Fund invests in and with its partnerships. In particular, the Fund expects Brunel to have a robust approach to conflicts of interest. This includes having comprehensive controls operating at all levels within the business to prevent conflicts of interest from adversely affecting the interests of the Devon Pension Fund and other clients, including the Fund’s members and employers.

The effective management of potential Conflicts of Interest is a key component of Brunel’s due diligence on all asset managers and service providers, as well as ongoing contract management. Conflict of interest clauses are included in investment management agreements. Conflicts are also considered when undertaking voting and engagement. Details on how EOS at Federated Hermes, Brunel’s appointed engagement voting provider, approach conflicts of interest are available on their website.

(e) Data and Information

The Devon Pension Fund recognises that ESG data is a developing discipline and is a strong advocate for improved disclosure from companies and assets in which it invests. The Fund will use a variety of data sources to analyse the ESG risks of its investments and asset allocation strategy. It expects Brunel to use its own analysis and that of its asset managers to inform its stewardship activity and risk ESG management, as well as media and company reports and a variety of third party proprietary and public data sources.

Given the lack of standardisation and transparency across ESG data, differing methodologies can lead to different outputs and biases. On behalf of the DEvon Pension Fund and other clients, Brunel use a variety of best in class providers, which leverage the Sustainability Accounting Standards Board’s (SASB) materiality framework, to reduce bias, provide greater coverage of our assets, improve awareness of differences in data providers or to aid specific targeted engagement priorities. SASB promotes better quality reporting on material ESG risks, the standards focus on financially material issues. Another framework Brunel endorses is the Task Force on Climate-related financial disclosures (TCFD) which has developed a set of consistent climate-related financial disclosures that can be used by companies. Further detail on the TCFD is located in Brunel’s Responsible Investment Policy and Climate Change Policy.

These sources of data are embedded into quarterly reports reviewed by Brunel at quarterly Brunel Investment Risk Committee meetings and are included in the reports provided to the Devon Investment and Pension Fund Committee.

The Fund recognises that data provision is a continuously evolving area. The Fund supports Brunel’s policy of reviewing their use of providers annually and providing feedback where developments could be made. Brunel seek to stimulate market-wide improvements in ESG risk analysis and commit to continue to innovate, adapt and improve to ensure the availability of robust, independent and effective data to work collegiately with external asset managers on the management of the whole spectrum of investment risks.

(f) Voting

Responsibility for the exercise of voting rights has been delegated to the Brunel Pension Partnership. For the Brunel passive portfolios, Brunel have further delegated voting to Legal and General Investment Management, but have retained the right to direct split voting on significant issues.

Brunel have adopted voting guidelines, following extensive consultation with their client funds, which can be found on their website.

The Devon Pension Fund requires that Brunel will always seek to exercise its rights as shareholders through voting. This means seeking to vote 100% of available ballots. However, as with any process, errors and issues can occur. If the level of voting drops below 95% this would raise a cause for concern, be investigated and corrective action identified.

Votes should be cast applying the following principles:

- Consistency: Brunel should vote consistently on issues, in line with their Voting Policy, applying due care and diligence, allowing for case-by-case assessment of companies and market-specific factors. This should include consideration of engagement with companies when voting.

- No abstention: Brunel should aim to always vote either in favour or against a resolution and only to abstain in exceptional circumstances or for technical reasons, such as where a vote is conflicted, a resolution is to be withdrawn, or there is insufficient information upon which to base a decision.

- Supportive: Brunel should aim to be knowledgeable about companies with whom they engage and to always be constructive. Brunel should aim to support boards and management where their actions are consistent with protecting long-term shareholder value.

- Long-term: Brunel should seek to protect and optimise long-term value for shareholders, stakeholders and society.

- Engagement: Brunel should support aligning voting decisions with company engagement, and escalate the vote if concerns have been raised and not addressed in the prior year.

- Transparency: The Devon Pension Fund expects Brunel to be transparent and publish voting activity no less than twice per year.

The Devon Pension Fund expects that companies will conduct themselves as follows:

- Accountability: The directors of a company must be accountable to its shareholders and make themselves available for dialogue with shareholders.

- Transparency: We expect companies to be transparent and to disclose, in a timely and comprehensible manner, information to enable well-informed investment decisions. This includes environmental and social issues that could have a material impact on the company’s long-term performance.

- One Share, One Vote: We support one share, one vote. Where a company issues shares with differing rights, they must define these rights transparently and clearly explain why rights are not equal.

- Informed votes: We expect companies to make complete materials for general meetings available to shareholders and, where possible, to do so in advance of the legal timeframes for the meeting.

- Development: We encourage companies to explore technology to improve the voting process and confirmation, such as blockchain, virtual meetings, electronic voting, and split voting (ownership proportion).

The Devon Pension Fund is a member of the Local Authority Pension Fund Forum (LAPFF). LAPFF also conducts significant engagement with companies on behalf of their member funds, and where there is a significant issue to be voted on at a company AGM they will issue a voting alert, with a recommendation to member funds on how to vote.

Where a voting alert has been issued by LAPFF, the Devon Pension Fund expects that Brunel (and Legal and General Investment Management) should give consideration to LAPFF’s recommendation when deciding how to vote. Brunel should report back to the Fund on how they have voted and the rationale for their vote, especially where they vote differently to the LAPFF recommendation.

In exceptional circumstances, the Devon Pension Fund may direct a split vote where the Fund has a specific investment policy commitment. Brunel has made provisions to allow clients, by exception, to direct votes, including the passive pooled funds, as an elective service. Client funds need to submit the request in line with the issuance of the meeting notification, usually not less than 2-3 weeks prior to an AGM/EGM.

The following issues are of particular concern to the Devon Pension Fund in determining how shares should be voted. The Fund’s policies on these issues align with Brunel’s voting guidelines, which are not repeated in full here, but more details can be on the Brunel’s website.

Sustainability

Companies should effectively manage environmental and social factors, in pursuit of enhancing their sustainability.

A company’s governance, social and environmental practices should meet or exceed the standards of its market regulations and general practices and should take into account relevant factors that may significantly impact the company’s long-term value creation. Issuers should recognise constructive engagement as both a right and a responsibility.

Human and Natural Capital

Companies operate interdependently with the economy, society, and the physical environment. The availability and retention of an appropriately skilled workforce will impact company productivity. Similarly, companies impact the environment through their use of natural resources e.g. water, waste and raw materials. The physical environment has an impact too; extreme weather can disrupt supply chains, either directly or indirectly which can impact company productivity.

Companies should manage their workforce and natural capital effectively to enhance their productivity and to deliver sustainable returns. Companies should regularly disclose key metrics on their capital requirements and risks. Directors of companies should be accountable to shareholders for the management of material environmental and social risks which, over the long term, will affect value and the ability of companies to achieve long term returns.

Company Boards – Conduct and Culture

Corporate culture and conduct have always been important, but recent evidence from incidents where conduct has fallen below the expected standards has reinforced the need to focus on conduct and culture, as well as highlighting the financial risks linked to low standards on conduct.

Board Composition and Effectiveness

The composition and effectiveness of boards is crucial to determining company performance. Boards should comprise a diverse range of skills, knowledge, and experience, including leadership skills, good group dynamics, relevant technical expertise and sufficient independence and strength of character to challenge executive management and hold it to account.

The Devon Pension Fund believes that to function and perform optimally, companies and their boards should seek diversity of membership. They should consider the company’s long-term strategic direction, business model, employees, customers, suppliers and geographic footprint, and seek to reflect the diversity of society, including across race, gender, skill levels, nationality and background. Robust succession planning at the Board and senior management level is vital to safeguard long-term value for any organisation, including planning for both unanticipated and foreseeable changes.

The board is accountable to shareholders and should maintain ongoing dialogue with its long-term shareholders on matters relating to strategy, performance, governance and risk and opportunities relating to environmental and social issues. This dialogue should support, but not be limited to, informing voting decisions at annual meetings.

Executive Remuneration

Executive remuneration is a critical factor in ensuring management is appropriately incentivised and aligned with the best interests of the long-term owners of the business. Whilst judgement of remuneration is therefore made on a case-by-case basis, we adhere to the following guiding principles:

- Simplicity: pay schemes should be clear and understandable for investors as well as executives.

- Shareholding: the executive management team should make material investments in the company’s shares and become long-term stakeholders in the company’s success.

- Alignment and quantum: pay should be aligned to the long-term success of the company and the desired corporate culture and is likely to be best achieved through long-term share ownership.

- Accountability: remuneration committees should use discretion to ensure that pay properly reflects business performance. Pay should reflect outcomes for long-term investors and take account of any decrease in the value of or drop in the reputation of the company.

- Stewardship: companies and investors should regularly discuss strategy, long-term performance and the link to executive remuneration.

- Behaviour: the most senior executives should willingly embrace the approach described. If they do not, boards should consider the implications.

Audit

The audit process is vital to ensuring the integrity of company reporting and the presentation of a true and fair view, enabling shareholders to assess the financial health and long-term viability of a company.

Protection of Shareholder and Bondholder Rights

The rights of shareholders and bondholders should be protected, including the right to access information, to receive equal treatment and to propose resolutions and vote at shareholder meetings. We support a single share class structure and generally oppose any measures to increase the complexity of shareholding structures. We will generally require the unbundling of resolutions, giving shareholders the right to vote distinctly on the general, and enhanced authorities to issue shares as separate items on the agenda of shareholder meetings. We also support adherence to the highest possible standards on listed stock exchanges.

(g) Stock Lending and Share Recall

The Devon Pension Fund permits holdings in its segregated portfolios to be lent out to market participants. Stock lending is an important factor in the investment decision, providing opportunities for additional return, but that lending should not undermine governance, our ability to vote or long-term investing. The stock lending programme is managed by Brunel, and the Fund adopts Brunel’s policies on stock lending and share recall.

Voting rights attached to a stock or security reside with the borrower for as long as it is out on loan. Stock will be recalled from stock lending where Brunel considers it in the client’s best interest and consistent with our investment principles.

Where there is a perceived trade-off between the economic benefit of stock lending, and Brunel’s ability to discharge its obligations as a responsible long-term investor, the latter will have precedence. Securities lending entails operational process risks such as settlement failures or delays in the settlement of instructions. The Devon Pension Fund expects Brunel to undertake a comprehensive review of the potential risks and implemented measures to mitigate and reduce the risk. Controls include, but are not limited to:

- An approved borrowers list.

- Retention of 5% of any one stock.

- On average, stock will be lent no longer than 21 days.

- Restrictions on acceptable collateral.

All measures and service level agreements are regularly monitored. Brunel examines the selection criteria for approved borrows to confirm consistency with Brunel’s internal requirements regarding appropriate criteria. The selection criteria and content of the Approved List will be reviewed by Brunel at least annually.

There may be some instances where Brunel decides not to stock lend, for example where they have co-filed a shareholder resolution, but particularly where there are concerns of borrowers deliberately entering transactions to sway the outcome of a shareholder vote.

The decision to stock lend is a collective decision made by Brunel’s clients and is supported by the Devon Pension Fund. Stock lending is applied at portfolio level and reviewed annually as part of the product governance cycle. The policy and relevant SLAs are also reviewed annually. Brunel’s approach to responsible stock lending is outlined in further detail in a separate policy.

(h) Fixed Interest and Diversifying Returns Funds

Fixed interest instruments are debt instruments and therefore do not usually confer voting rights. However, in relation to corporate bonds, the Devon Pension Fund believes that well-governed companies are more likely to make their loan repayments and improve their creditworthiness, enabling better access to funds to support the creation of long-term value for shareholders, other stakeholders, society, and the environment.

Where voting rights are not attached and where opportunity to engage is limited, stewardship focuses on the managers’ investment decision-making. The Devon Pension Fund expects Brunel to integrate Environmental Social and Governance (ESG) considerations into manager selection and ongoing manager monitoring to ensure that ESG is imbedded into the investment process at an issuer, sector, and geographic level.

Where voting rights are attached to fixed income, the Devon Pension Fund, via Brunel, will have the opportunity to vote at company meetings (AGM/EGMs). The Fund would look to Brunel to engage particularly prior to issuance, where the most impact can be made. However, we recognise that there is more work to be done in this asset class.

Diversified returns funds incorporate a wide range of investment strategies and multi asset funds providing diversification. Investors own units in these funds rather than owning the underlying holdings directly. Stewardship focuses on the managers investment decision-making.

(i) Private Markets

Stewardship is an intrinsic part of private markets investing due to the degree of influence and control, lack of short-term results pressure on capital markets, and long-term nature of the investments that are made. There are however some natural barriers to stewardship due to the lack of disclosure and often opaque nature of the asset classes and arm’s length relationships between general partners (GPs) and limited partners (LPs). As a result, in-depth due diligence is critical, alongside building close relationships and exerting influence where possible.

When assessing potential private market investments, the Devon Pension Fund would expect Brunel to pay particular attention to ESG and sustainability throughout the selection process. We believe that well governed investments and those with strong ESG and sustainability characteristics will offer better long-term risk-adjusted returns.

Managers should have firm ESG and climate change policies in place, and these should be considered across the value chain, from investment due diligence to ongoing managing, monitoring, and ultimately disposal of the assets. As part of this due diligence Brunel examine case studies to evidence these policies are in place and, crucially, are being actioned. Proof of implementation is critical and supersedes all else. The Devon Pension Fund and Brunel will support managers on their journey and encourage best practice, forgiving policies and processes not being formalised so long as the manager commits to action in a reasonable timeframe.

Application of robust stewardship in private markets is very dynamic. Brunel seeks to use the appropriate mechanisms relative to the asset class, size and complexity of the investment, position in the capital structure and the influence that does or does not permit.

Stewardship actions across private markets include;

- Ensuring appropriate governance structures are in place, with particular attention paid where managers have minority positions in assets.

- Assessing the manager’s approach to diversity and inclusion and where possible tracking metrics to substantiate claims.

- Assessing the manager’s knowledge and commitment to Responsible Investment and climate change mitigation and avoidance.

- Assessing how Responsible Investment is integrated into the investment and asset management processes and fully embedded in the culture of the organisation (both deal teams and operations teams), or whether this is siloed in a separate ESG team.

- Supporting the manager’s ongoing development of their Responsible Investment and Stewardship practices, including where appropriate participation in events, workshops as a representative on the Limited Partner Advisory Committee (LPAC).

- Establishing what commitments to Responsible Investment through existing or planned memberships/affiliations with organisations such as Principles for Responsible Investment (PRI), TCFD, GRESB and/or have adopted the SASB framework.

- Assessing the awareness, training, capacity and track record on Responsible Investment issues.

- Working with managers to improve transparency and quality of the manager’s ESG approach and reporting.

Further details of Brunel’s approach to private markets are included in the Brunel Stewardship Policy.

(j) Reporting

The Investment and Pension Fund Committee will monitor Brunel’s engagement with the companies they have invested in, through the regular reporting arrangements in place. Brunel and LGIM’s voting records will be reported to Committee on a quarterly basis. The engagement activity undertaken by Brunel and LAPFF will also be reported to Committee on a quarterly basis, together with a record of voting alerts issued by LAPFF, how Brunel and LGIM have voted on the proposals concerned and the outcome of the votes.

The Devon Pension Fund Annual Report each year includes a report focusing on stewardship and voting activity. This will include details of investment manager activity, voting analysis, LAPFF alert analysis, engagement, case studies and collaboration. A summary of Brunel’s stewardship activities is also included.

7. Advice Taken

This Investment Strategy Statement has been put together by Devon County Council’s professional investment officers, supported by the Fund’s Independent Investment Advisor, and with advice from Redington investment advisors, who have conducted a review of the Fund’s investment strategy and asset allocation. Redington were appointed to conduct the most recent review in 2025 following a procurement exercise under the relevant South West LGPS Framework. Previous reviews in 2022 and 2019 were carried out by Mercer LLC. For the 2025 review, strategic objectives were set in line with Part 7 of the Investment Consultancy and Fiduciary Management Market Investigation Order 2019, issued by the Competition and Markets Authority.

The Devon Pension Fund has committed to pooling investments through the Brunel Pension Partnership Limited (BPP Ltd.), and advice from both Brunel and the Brunel Client Officer Group project team has also been taken into account in shaping the Devon Pension Fund response to the pooling initiative and building an investment strategy that can be implemented via Brunel.

The key people who have been consulted and who have provided advice in drawing up the Investment Strategy Statement are:

The Investment and Pension Fund Committee

This Devon County Council Committee, which includes Unitary and District Council and other employer representatives and those of the contributors and the pensioners, carries out the role of the Administering Authority. It has full delegated authority to make decisions on Pension Fund matters. In particular it:

- decides the Investment Principles;

- determines the fund management structure;

- reviews investment performance.

The Devon Pension Board

While not a decision making body, the Pension Board has been set up to assist the Administering Authority in securing compliance with legislation and regulation and the effective and efficient governance of the Fund. Members of the Pension Board were included in a consultation workshop on the investment strategy, and regularly review the Fund’s statutory statements.

Devon County Council Director of Finance and Public Value: Angie Sinclair CPFA

The Director of Finance and Public Value advises the Investments and Pension Fund Committee and ensures that it is informed of regulatory changes and new developments in the investment field and implements the committee’s decisions. Angie Sinclair is a CIPFA qualified accountant and has been the Director of Finance and Public Value and Section 151 Officer for Devon County Council since Autumn 2021, and has worked for the Council since 2007. Angie has responsibility for Devon County Council’s finances, including responsibility for the Devon Pension Fund. Angie is a Chartered Certified Accountant and Chartered Institute of Public Finance Accountant (CIPFA) giving her an insight into both public and private sector accounting.

Devon County Council Head of Investments: Mark Gayler ACMA, IMC

Mark Gayler has been Head of Investments (previously titled Assistant County Treasurer, Investments and Treasury Management) at Devon County Council since 2013. Mark heads up the investment team responsible for overseeing the Devon Pension Fund, as well as undertaking treasury management for the council. Mark also oversees Peninsula Pensions, the shared pension administration service. Mark is a CIMA qualified accountant and holds the CFA Level 4 Certificate in Investment Management. Mark has over 35 years of experience within local government, and first moved to the Investment Team in 2010, initially as Deputy Investment Manager.

Devon County Council Investment Manager: Charlotte Thompson APMI

Charlotte Thompson has worked as Investment Manager in the Investment Team since June 2018, having transferred from her previous role as Head of Peninsula Pensions. She has over 25 years’ experience in the Pensions Industry. Prior to joining Devon County Council, Charlotte worked for Friends Provident, managing a portfolio of defined benefit schemes. She is an associate of the Pensions Management Institute, and is also currently studying for the Investment Management Certificate.

Independent Investment Advisor: Anthony Fletcher, MJ Hudson Allenbridge

Anthony is the independent adviser to the Devon County Council Investment and Investment and Pension Fund Committee. He also acts as advisor to the Derbyshire, Surrey and Wiltshire pension funds. He has over 30 years’ investment experience, and has had FCA Approved Person status throughout his career: – currently FCA CF30 Investment Advice. His last full-time role was with Aberdeen Asset Management, where he was a Fixed Income Portfolio Manager and was responsible for twenty four pan-European and global fixed income institutional client portfolios. This included insurance company assets and charitable foundations; UK corporate and local authority DB and DC pension funds and sovereign wealth funds, with a combined AUM of £3.6 billion, and four pooled funds with assets of a further £460 million.

Redlington Investment Consultants

Jill Davys, Head of LGPS

Jill has been the Head of LGPS at Redington for 3 years and advises several LGPS clients. Jill initially worked for 20 years in the City as a Fund Manager at both in-house pension funds and fund managers. Her primary focus was on equities; however, she was also involved in investment strategy and derivatives. Jill then worked directly in the LGPS for 18 years at a range of Funds at a senior level. In these roles she was responsible for managing all aspects of the Funds, including investment strategy, responsible investment and the relationship with the investment pool company.

Kieran Harkin

Kieran has 24 years of industry experience and joined Redington 2 years ago, having worked closely with the LGPS in previous roles. Kieran has advised multiple LGPS funds and has extensive experience of advising in respect of strategic and tactical asset allocation, risk management and sustainable investment paired with strong stakeholder communication and engagement skills. Kieran is a voting member of Redington’s Investment Strategy Committee.

Charlie Sheridan

Charlie joined Redington 7 years ago and has worked closely with a number of LGPS Funds as well as pools over that time. He works as a senior supporting consultant to a number of LGPS Funds, working closely with Jill and other lead consultants to deliver advice. Charlie has been a key part of the work delivered to LGPS clients across investment strategy reviews, responsible investment, manager selection and implementation. He has played a significant role in the formulation of advice as well as delivery to Officers and Committees.

Brunel Pension Partnership

The Brunel Pension Partnership now manages the majority of the Devon pension Fund’s investment mandates. Brunel provides specifications for each of its portfolios operational, agreed across its client funds, and these specifications enable the Fund to determine how each portfolio fits into the Fund’s investment strategy. The Brunel Responsible Investment Team has also provided significant advice and support on the development of the Fund’s approach to stewardship and climate change.

Brunel Client Officer Group

The Brunel Client Officer Group has provided support with regard to the impact on strategy of the investment pooling proposals. The group comprises the investment officers from the Avon Pension Fund (Bath and NE Somerset Council), Buckinghamshire CC, Cornwall Council, Devon CC, Dorset Council, Gloucestershire CC, Oxfordshire CC, Somerset CC, Wiltshire Council and the Environment Agency.

Annex 1 – Compliance with the Myners Principles

The Investment and Pension Committee has considered the 6 Myners Principles and is of the view that the Fund currently complies with the spirit of these recommendations. Further details are given below on each of the 6 principles.

1. Effective Decision Making

The Devon County Council has a designated Committee whose terms of reference are to discharge the duties of the Council as the Administering Authority. There is a training programme for Committee members. They also have external and internal advisers and are supported by an experienced in-house team to oversee the day to day running of the Fund. Representatives of the Devon Pension Fund’s contributors and pensioners, who have one collective vote, advise the committee on the views of their members. The Administering Authority is supported by a Pension Board, whose role is to assist them in securing compliance with legislation and regulation and the effective and efficient governance of the Fund.

2. Clear Objectives

This document sets out clear objectives in relation to the split of assets between equities and bonds, investment in diversified growth funds, and other assets such as property.

The Investment and Pension Committee is aware of the Devon Pension Fund’s current actuarial deficit and its investment policy is designed to gradually improve solvency whilst keeping employers’ contribution rates as constant as possible. A key objective of the Fund’s strategy is to manage the Fund to ensure a healthy cash-flow for the foreseeable future.

3. Risk and Liabilities

The Investment and Pension Committee has considered the mix of assets that it should adopt and the level of risk (volatility of returns) it is prepared to accept. This document sets out current policy, which is designed to improve the Fund’s solvency while only accepting moderate risk.

The Investment and Pension Committee will regularly review the benefits of using the full range of asset classes.

4. Performance Assessment

In the allocation of funds to individual portfolios provided by the Brunel Pension Partnership, benchmarks have been set for each asset class, as set out in Annex 2. The total fund is measured against a bespoke benchmark based on the Devon Pension Fund’s strategic asset allocation.

The Devon Pension Fund uses the services of its custodian bank to provide an independent measurement of investment returns. These are used for comparison purposes against specific and peer group benchmarks.

The Investment and Pension Fund Committee receive quarterly performance reports and are therefore able to consider the performance of all asset classes and managers on a regular basis, focusing on the longer term. These considerations form the basis of decision making.

5. Responsible Ownership

The Stewardship secion of this document, on the policy of the exercise of rights (including voting rights) attaching to investments, sets out the Devon Pension Fund’s commitment to responsible ownership. The services agreement with the Brunel Pension Partnership includes provision for them to engage with companies in compliance with the terms of the Combined Code and the Council’s voting policy as set out in this document. Brunel have published their stewardship and voting policies which are referenced in this document. The Fund is also a member of the Local Authority Pension Fund Forum (LAPFF). This document sets out the Council’s policy on voting.

6. Transparency and Reporting

This Investment Strategy Statement is available to any interested party on request. The latest version is available on the Devon Pension Fund website.

In accordance with LGPS (Administration) Regulations 2008, the Devon Pension Fund has published a Communications Policy Statement which describes the Devon Pension Fund’s policy on:

- Providing information to members, employers and representatives.

- The format, frequency and method of distributing such information.

- The promotion of the Fund to prospective members and their employing bodies.

The Fund will continue to develop the Devon Pension Fund website, which it considers to be its primary communications channel.

Annex 2 – Current Managers and Mandates

Brunel Mandates

| Mandate | Mnagers | Target |

|---|---|---|

| Passive Paris Aligned Global Developed Equities | Legal and General Investment Management | Performance in line with the FTSE Global Developed Paris Aligned Benchmark |

| Global High Alpha Equities | Alliance Bernstein Baillie Gifford Fiera Capital Harris Associates Royal London | Outperform MSCI World TR Index by 2-3% per annum over a rolling 3-5 year period |

| Emerging Markets Equities | Ninety One Robeco Stewart Invs | Outperform MSCI Emerging Markets TR Index by 2-3% per annum over a rolling 3-5 year period |

| Global Smaller Company Equities | Montanaro Kempen American Century | To outperform the MSCI World Small Cap Index TR by 2% per annum over a rolling 3-5 year period |

| Sustainable Equities | Jupiter Ownership Capital Nordea RBC Global Asset Management Mirova | Outperform the MSCI All Country World Index (ACWI) TR Index by 2% per annum over the medium to longer term (3-5 years) |

| Index-Linked Gilts | Blackrock | FTSE Actuaries UK Index Linked Gilts Over 5 Years Index |

| Sterling Corporate Bonds | Royal London Asset Management | Outperform the MSCI All Country World Index (ACWI) TR Index by 2% per annum over the medium to longer term (3-5 years) |

| Sterling Corporate Bonds | Royal London Asset Management | Outperform Barclays Capital Global Aggregate Bond Index by 1% per annum |

| Multi Asset Credit | Neuberger Berman CQS Oaktree | Outperform GBP SONIA by 4-5% per annum over a rolling 3-5 year period |

| Diversifying Returns Fund | JP Morgan Fulcrum Lombard Odier UBS | Outperform GBP SONIA by 3-5% per annum over a rolling 5-7 year period |

| UK Property | Brunel Private Markets Team | Outperform the MSCI/AREF UK Quarterly Property Fund Index by 0.5% p.a. over a rolling 5 – 7 year period. |

| International Property | Brunel Private Markets Team | Outperform the MSCI Global Quarterly Property Fund Index by 0.5% p.a. over a rolling 5 – 7 year period. |

| Infrastructure | Brunel Private Markets Team Stepstone | Outperform the Consumer Prices Index + 4% |

| Private Equity | Brunel Private Markets Team Aksia | Outperform the MSCI All Country World Index by 3% p.a. over a rolling 7 – 10 year period. |

| Private Debt | Brunel Private Markets Team

Aksia | Outperform the Consumer Prices Index + 4% |

| Private Debt | Arcmont

Golub | Outperform the Consumer Prices Index + 4% |

DCC Investments Team Mandate

| Mandate | Managers | Mandate |