Contents

County Treasurer’s Report

Introduction

Over the course of the 2021/22 year, the value of the Devon Pension Fund increased from £5.035 billion (as at 31 March 2021) to £5.412 billion as at 31 March 2022.

The first nine months of the reporting period saw equity markets continuing to rise as the world continued to recover from the impact of the Covid-19 pandemic. After peaking in late December / early January global markets were then hit first by concerns over rising inflation and interest rates and then by geo-political concerns over Russia’s invasion of Ukraine. The last quarter therefore reduced the Devon Pension Fund’s investment return for the year, net of fees, down from +10.9% as at 31 December to +7.7% as at 31st March. While this was still a healthy positive return, it was below the Fund’s strategic benchmark of +9.3%, and also below the LGPS universe average of +8.2%.

Around 95% of the Fund’s investment assets are now managed by the Brunel Pension Partnership Ltd, a company set up to pool investment assets in order to reduce investment costs and improve risk management. Since the company was set up five years ago the Devon Fund has been gradually transitioning its investment assets. During the early Summer, the Fund transitioned its fixed interest investments, previously managed by Lazard Asset Management and Wellington Management, across to funds managed by Brunel. The Devon Pension Fund continues to be responsible for deciding the strategic allocation between different asset classes to meet local investment objectives, but the Brunel Pension Partnership undertakes the selection and monitoring of the external investment managers who manage the investments.

The administration of pension benefits is undertaken for the Devon Fund by Peninsula Pensions, a shared pensions administration service between Devon and Somerset. Peninsula Pensions continues to deliver strong performance for both members and employers. During 2021/22, the team has further reviewed and enhanced processes, developing technological solutions where appropriate, while remaining fully compliant with LGPS and other relevant regulations. The team is well positioned to manage future challenges and ensure compliance with future regulatory changes. The team has successfully adapted to revised working arrangements introduced as a result of COVID-19, making greater use of technology and electronic communication to maintain business as usual with no impact on service provision, despite the challenges of a significant increase in demand.

Summary of Financial Statements

The financial statements and their purpose are summarised as follows:`

- Fund Account – The Fund Account sets out the Pension Fund’s income and expenditure for the year to 31 March 2022. The first section sets out the income received in contributions from employers and employees, and the expenditure on pension benefit payments. The second section of the Fund Account shows the income received from the Fund’s investments and the cost of managing those investments. Investment income from property, infrastructure and private debt investments is returned as cash and can be used to offset any shortfall between contributions and benefit payments. The Fund’s equity and bond investments are made via pooled funds which retain and reinvest the income from the individual securities. The Fund Account also shows that there has been an increase in the capital values of the Fund’s investment assets of £380 million over the last year.

- Net Asset Statement – The Net Asset Statement sets out the net assets of the Fund, in line with the IFRS based Code of Practice on Local Authority Accounting in the United Kingdom (the Code) and the latest Statement of Recommended Practice (SORP). Pooled investments include pooled Equity, Fixed Interest, Property, Infrastructure and Private Debt Funds and they are incorporated into those categories in reviewing the Asset Allocation of the Fund in a later section of my report.

Investment Performance

As indicated above, the asset value of the Fund at the end of the 2021/22 financial year was £5.412 billion. This represents an investment return of +7.7% net of fees, compared with the Fund’s internally set strategic benchmark target of +9.3%.

The Fund’s strategic benchmark is set as an average of the benchmarks for each of the investment portfolios, weighted according to the Fund’s strategic asset allocation targets. Bond markets saw negative returns over the year as a result of increasing interest rates. The cash plus benchmark of the Brunel Multi-Asset Credit portfolio meant that the return of -1.5% was significantly below benchmark. Infrastructure was also below an inflation plus benchmark as inflation began to rise significantly.

Concerns over inflation and Russia’s invasion of Ukraine resulted in negative equity markets over the last quarter. The last quarter also saw poor relative performance by the active equity portfolios, with the exception of the Low Volatility portfolio. Brunel’s Global High Alpha and Sustainable Equities portfolios were both well below benchmark during a negative quarter when their investments in sustainable and “growth” companies did less well than “value” companies including the oil companies, whose share price went up as oil prices soared.

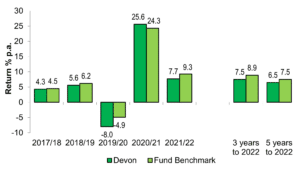

The following chart presents the investment returns achieved by the Devon Fund compared to the Fund’s benchmark over each of the last five years, plus the total annualised return over the last three years and the last five years. Performance Figures are shown net of fees.

Investment Performance Summary

Fund solvency

The Fund is required to have an actuarial valuation conducted every three years. The most recent triennial valuation, as at 31 March 2019, carried out by the Fund Actuary, Barnett Waddingham determined that the Devon Pension Fund had a funding level of 91%.

At the end of December 2021, a funding update provided by the Fund Actuary, based on rolling forward the data from the 2019 valuation, updating it for subsequent investment returns, pension and salary increases, and revised assumptions on future investment returns, suggested that the funding level was broadly similar at around 92%.

The annualised investment return over the last three years of +7.5% will have improved the Fund’s position, but this is offset by the Actuary assuming lower investment returns going forward.

However, work on the next scheduled triennial valuation, as at 31 March 2022, is now underway. The 2022 valuation will comprise a more detailed analysis and updating of the Fund’s liabilities, based on revised data as at 31 March 2022 and revised assumptions. The valuation has to be carried out in a way that ensures the solvency of the Fund and achieves long term cost efficiency in setting contribution levels to reduce the deficit in the funding position.

The Fund will have an ongoing dialogue with employers over the valuation period to ensure that any concerns they have about future contribution levels are addressed.

Asset allocation

The Investment and Pension Fund Committee is charged with the responsibility for governance and stewardship of the Fund and making decisions about strategic asset allocation policy.

During the year, some small changes were made to the asset allocation targets. The target allocation for sustainable equities was increased from 3% to 5%, funded by a reduction in passive equities. The Fund also began to build up an allocation to private equity, although it will take some time to achieve a meaningful allocation. Over the medium to long term it is proposed to build up all the private market allocations, funded from the current allocation to diversifying returns funds.

The Fund’s actual asset allocation as at 31 March 2022 is shown in the following chart:

Actual Asset Allocation as at 31 March 2022

A comparison of the actual allocation as at 31 March 2022 with the Fund’s target allocation for 2021/22 is shown in the following table:

Actual Asset Allocation Compared to Target

| Target allocation 31 March 2021 % | Actual allocation 31 March 2021 % | Target allocation 31 March 2022 % | Variation from Target % | ||

|---|---|---|---|---|---|

| Global Bonds | 7.0 | 6.0 | 7.0 | 6.1 | |

| Multi-Sector Credit | 7.0 | 6.8 | 7.0 | 7.2 | |

| Cash | 1.0 | 0.4 | 1.0 | 0.5 | |

| Total Fixed Interest | 15.0 | 13.2 | 15.0 | 13.8 | -1.2 |

| Passive Equities | 33.0 | 35.8 | 31.0 | 31.6 | |

| Active Global Equities | 5.0 | 6.3 | 5.0 | 5.5 | |

| Active Small Cap Equities | 5.0 | 5.7 | 5.0 | 5.3 | |

| Active Sustainable Equities | 3.0 | 3.0 | 5.0 | 4.8 | |

| Active Emerging Market Equities | 5.0 | 5.6 | 5.0 | 4.6 | |

| Active Low Volatility Equities | 7.0 | 6.7 | 7.0 | 7.2 | |

| Total Equities | 58.0 | 63.1 | 58.0 | 59.0 | +1.0 |

| Diversified Growth Funds | 8.0 | 9.5 | 7.0 | 9.3 | |

| Property | 10.0 | 8.1 | 10.0 | 9.4 | |

| Infrastructure | 6.0 | 4.0 | 6.0 | 6.0 | |

| Private Equity | – | – | 1.0 | 0.5 | |

| Private Debt | 3.0 | 2.1 | 3.0 | 2.0 | |

| Total Alternatives/Other | 27.0 | 23.7 | 27.0 | 27.2 | +0.2 |

Following a review undertaken by Mercer investment consultants in February 2022, further changes are proposed for 2022/23, as follows:

- An increase in the allocation to Multi-Sector Credit to 12%, making a total allocation to Fixed Interest of 20%.

- A reduction in the overall allocation to Equities to 50% of the Fund to reduce risk.

- Within Equities, termination of the allocation to Low Volatility, a reduction in Passive Equities and an increase in the allocation to Sustainable Equities from 5% to 10%.

- An increase in the medium-term target for each of Private Debt and Private Equity to 5%.

These changes should allow the Fund to achieve the required level of return, but at a reduced level of risk.

Conclusion

It is disappointing that for the second time in three years events over the last quarter have led to a below benchmark return. Two years ago, it was Covid, this year it has been concerns over rising inflation and the impact of Russia’s invasion of Ukraine.

Nevertheless, the annualised investment return of 7.5% over the last three years has exceeded the Actuary’s assumption, which should stand us in good stead for the triennial valuation.

Although performance was behind benchmark, this resulted from market conditions where oil companies and banks performed well, and more sustainable growth companies performed badly. Our responsible investment policy, implemented in partnership with Brunel meant that we had less of the former and more of the latter than the benchmark indices. This should be a blip and a trend that should reverse as the world takes more action to combat climate change.

Peninsula Pensions, the shared service that administers pension benefits for both the Devon and Somerset Pension Funds, continues to perform well. It is good to see regular compliments being received from pension fund members about the service they receive.

The Fund remains committed to ensuring that it provides an excellent service to pension fund members and value for money for both pension fund members and local taxpayers.

Angie Sinclair

Director of Finance and Public Value

Summary Pension Fund Accounts

Fund Account

| 2021 £000 | 2022 £000 | |

|---|---|---|

| Contributions and benefits | ||

| Contributions receivable: | ||

| Employers | 171,456 | 128,172 |

| Employees | 42,805 | 45,260 |

| Transfers in from other schemes | 12,970 | 13,324 |

| Total | 227,231 | 186,756 |

| Benefits Payable | ||

| Pensions | (163,522) | (168,391) |

| Lump Sums | (24,617) | (29,018) |

| Death Benefits | (4,300) | (3,623) |

| Refunds | (586) | (596) |

| Transfers out to other schemes | (7,851) | (26,037) |

| Total | (200,876) | (227,665) |

| 26,355 | (40,909) | |

| Management Expenses | (20,791) | (28,453) |

| Return on Investments: | ||

| Investment Income | 35,020 | 33,647 |

| Change in market value of Investments | 1,015,231 | 380,768 |

| Net Return on Investments | 1,050,251 | 414,415 |

| Net Increase (Decrease) in the Fund during the year | 1,055,815 | 345,052 |

| Add: Opening Net Assets of the Fund as at 1 April | 4,011,115 | 5,066,930 |

| Net Assets of the Fund as at 31 March | 5,066,930 | 5,411,982 |

Net Asset Statement

| 2021 £’000 | 2022 £’000 | |

|---|---|---|

| Investments at Market Value | ||

| Long Term Investments | 768 | 838 |

| Fixed Interest | ||

| UK Public Sector Bonds | 11,144 | 0 |

| Overseas Government Bonds | 160,893 | 0 |

| Corporate Bonds – Global | 119,187 | 0 |

| Pooled Investments | 4,296,164 | 4,883,580 |

| Pooled Property Investments | 404,962 | 453,953 |

| Derivatives | 4,960 | (2,303) |

| Foreign Currency | 11,509 | 13,908 |

| Short Term Deposits and Cash Equivalents | 19,011 | 8,457 |

| Cash and Bank Deposits | 27,220 | 53,680 |

| Investment Payables and Receivables | 477 | (10,253) |

| Total | 5,056,295 | 5,401,860 |

| Long Term and Current Assets | 18,063 | 18,350 |

| Long Term and Current Liabilities | (7,428) | (8,228) |

| Net Assets of the Fund as at 31 March | 5,066,930 | 5,411,982 |

Current Investment Managers

Managers and Mandates

| Market Value 31 March 2022 £’000 | % of Total Investments % | |

|---|---|---|

| Brunel Pension Partnership | ||

| Passive Equities | 1,709,091 | 31.6 |

| Global High Alpha Equities | 295,699 | 5.5 |

| Global Small Cap Equities | 289,118 | 5.4 |

| Emerging Market Equities | 249,457 | 4.6 |

| Sustainable Equities | 258,166 | 4.8 |

| Low Volatility Equities | 391,135 | 7.2 |

| Sterling Corporate Bonds | 330,866 | 6.1 |

| Multi-Asset Credit | 392,082 | 7.3 |

| Diversifying Returns Fund | 502,440 | 9.3 |

| Property | 508,227 | 9.4 |

| Infrastructure | 186,296 | 3.4 |

| Private Equity | 25,448 | 0.5 |

| Private Debt | 17,434 | 0.3 |

| DCC Investment Team | ||

| Infrastructure | 138,838 | 2.6 |

| Private Debt | 91,022 | 1.7 |

| Cash | 16,541 | 0.3 |