Contents

Report of the Director of Finance and Public Value

Introduction

2022/23 has been a difficult year for investment markets. Geo-political concerns following Russia’s invasion of Ukraine, along with rising inflation and interest rates, have weighed heavily over investment markets. Under the circumstances the investment return for the year of -1.5% could have been worse. The value of the Devon Pension Fund fell from £5.412 billion, as at 31 March 2022, to £5.313 billion as at 31 March 2023. The Fund’s investment return was below the Fund’s strategic benchmark (a weighted average of the underlying benchmarks) of +0.9% but compared well with the median LGPS universe return of -3.3%.

During the first quarter of the year, we implemented changes to our investment strategy, reducing our equity exposure and increasing our exposure to fixed interest and our commitment to private markets. This was done with the intention of reducing risk but maintaining the return potential of our investments. The majority of our investments continue to be managed by the Brunel Pension Partnership who undertake the selection and monitoring of the external investment managers who manage the portfolios that we choose to invest in. While we aim to maximise the investment return at an appropriate level of risk, we also work in partnership with Brunel to act as good stewards of the shares in which we invest and manage the climate impact of our investments. During the year we were re-accredited as signatories of the UK Stewardship Code for our work in this area.

The administration of pension benefits is undertaken for the Devon Fund by Peninsula Pensions, a shared pensions administration service between Devon and Somerset. Peninsula Pensions continues to deliver strong performance for both members and employers despite the challenges of an ongoing increase in demand, alongside staff recruitment. During 2022/23, the team has introduced further technological solutions relating to payment of member pensions, and data provision from employers; and has other new developments in progress relating to the members online portal. The team is well positioned to manage future challenges, specifically the McCloud remedy and introduction of the Pension Dashboard, whilst ensuring compliance with both current and future LGPS amendments in conjunction with any other relevant regulatory changes. The team has successfully adapted to hybrid working arrangements in line with business needs following COVID-19 and continues to encourage the more efficient use of electronic communication.

Summary of Financial Statements

The financial statements and their purpose are summarised as follows:

Fund Account

The Fund Account sets out the Pension Fund’s income and expenditure for the year to 31 March 2023. The first section sets out the income received in contributions from employers and employees, and the expenditure on pension benefit payments. The second section of the Fund Account shows the income received from the Fund’s investments and the cost of managing those investments. Investment income from property, infrastructure and private debt investments is returned as cash and can be used to offset any shortfall between contributions and benefit payments. The Fund’s equity and bond investments are made via pooled funds which retain and reinvest the income from the individual securities. The Fund Account also shows that there has been a decrease in the capital values of the Fund’s investment assets of £95 million over the last year.

Net Asset Statement

The Net Asset Statement sets out the net assets of the Fund, in line with the IFRS based Code of Practice on Local Authority Accounting in the United Kingdom (the Code) and the latest Statement of Recommended Practice (SORP). Pooled investments include pooled Equity, Fixed Interest, Property, Infrastructure and Private Debt Funds and they are incorporated into those categories in reviewing the Asset Allocation of the Fund in a later section of my report.

Investment Performance

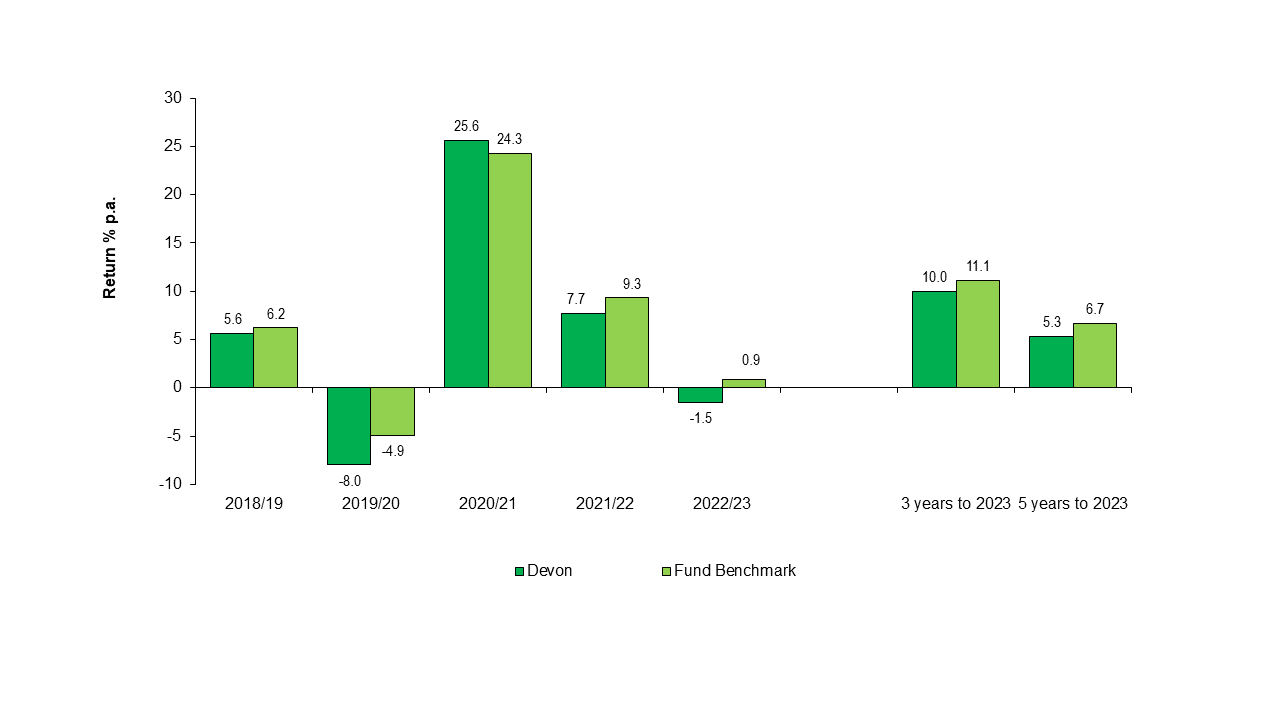

As indicated above, the asset value of the Fund at the end of the 2021/22 financial year was £5.412 billion. This represents an investment return of +7.7% net of fees, compared with the Fund’s internally set strategic benchmark target of +9.3%.

The Fund’s strategic benchmark is set as an average of the benchmarks for each of the investment portfolios, weighted according to the Fund’s strategic asset allocation targets. Bond markets saw negative returns over the year as a result of increasing interest rates. The cash plus benchmark of the Brunel Multi-Asset Credit portfolio meant that the return of -1.5% was significantly below benchmark. Infrastructure was also below an inflation plus benchmark as inflation began to rise significantly.

Concerns over inflation and Russia’s invasion of Ukraine resulted in negative equity markets over the last quarter. The last quarter also saw poor relative performance by the active equity portfolios, with the exception of the Low Volatility portfolio. Brunel’s Global High Alpha and Sustainable Equities portfolios were both well below benchmark during a negative quarter when their investments in sustainable and “growth” companies did less well than “value” companies including the oil companies, whose share price went up as oil prices soared.

The following chart presents the investment returns achieved by the Devon Fund compared to the Fund’s benchmark over each of the last five years, plus the total annualised return over the last three years and the last five years. Performance Figures are shown net of fees.

Fund solvency

The Fund is required to have an actuarial valuation conducted every three years. The most recent triennial valuation, as at 31 March 2022, has been carried out by the Fund Actuary, Barnett Waddingham over the last year. The valuation determined that the Devon Pension Fund’s funding level had improved from 91% to 98%, compared with the previous 2019 valuation.

The results of the 2022 actuarial valuation have been prepared in accordance with the current legislative arrangements for the Fund, taking into account revised financial assumption and longevity projections, as set out in the Funding Strategy Statement. The Fund’s assets were valued at £5,316 million against future pension liabilities assessed at £5,405 million, giving a deficit for this valuation of £89 million. The maximum deficit recovery period for any employer in the Fund has been set at 15 years, which is a reduction of 6 years from the previous valuation. The improvement in the funding level and reduction of the deficit recovery period showed good progress towards the long-term objective of 100% solvency.

However, the Fund Actuary has reassessed the position as at 31 March 2023, using the approach of rolling forward the data from the 2022 valuation, and updating it for subsequent investment returns, pension and salary increases. While it is not possible to assess the accuracy of the estimated liability as at 31 March 2023 without completing a full valuation, the results will be indicative of the underlying position. As a result of the negative investment return during 2022/23, compared with the Actuarial assumption of a 4.7% return, the Actuary has estimated that on a smoothed basis, considering market conditions as at 31 March 2023, the funding level will have deteriorated to around 93%.

Asset allocation

The Investment and Pension Fund Committee is charged with the responsibility for governance and stewardship of the Fund and making decisions about strategic asset allocation policy.

Following the review of investment strategy, carried out by Mercer during early 2022, some changes were made to the investment strategy with a view to reducing risk while maintaining a similar level of return. The allocation to equities was reduced from 58% to 50%. As part of the change, the previous allocation to low volatility equities was removed, on the basis that equity risk was better managed by reducing the total equity allocation rather than having a low volatility allocation. The passive allocation was reduced to 50%, half of the total equity allocation. The allocation to Sustainable Equities was increased to 10% in line with the Fund’s climate change policies and to better manage ESG (Environmental, Social and Governance) risk.

The allocation to fixed interest was increased to 20%. This was achieved by an increase of 5% to multi-asset credit, which is the riskier end of the fixed interest market but will still provide some diversification from equities. The medium-term allocation to private markets was increased to 30%, but with an adjustment to the 2022/23 allocation. This reflects the reality that private market investments take some time to build up and a short term allocation to diversified returns funds would be required to hold the funds to be drawn to fund private markets commitments.

Asset Allocation at 31.March 2023

A comparison of the actual allocation as at 31 March 2023 with the Fund’s target allocation for 2022/23 is shown in the following table:

Actual Asset Allocation Compared to Target

| Target allocation 31 March 2022 % | Actual allocation 31 March 2022 % | Target allocation 31 March 2023 % | Actual allocation 31 March 2023 % | Variation from Target % | |

|---|---|---|---|---|---|

| Sterling Corporate Bonds | 7.0 | 6.1 | 7.0 | 6.6 | |

| Multi-Sector Credit | 7.0 | 7.3 | 12.0 | 12.0 | |

| Cash | 1.0 | 0.5 | 1.0 | 1.2 | |

| Total Fixed Interest | 15.0 | 13.9 | 20.0 | 19.8 | -0.2 |

| Passive Equities | 31.0 | 31.6 | 25.0 | 26.5 | |

| Active Global Equities | 5.0 | 5.5 | 5.0 | 5.6 | |

| Active Small Cap Equities | 5.0 | 5.3 | 5.0 | 5.3 | |

| Active Sustainable Equities | 5.0 | 4.8 | 10.0 | 9.8 | |

| Active Emerging Market Equities | 5.0 | 4.6 | 5.0 | 4.5 | |

| Active Low Volatility Equities | 7.0 | 7.2 | 0 | 0 | |

| Total Equities | 58.0 | 59.0 | 50.0 | 51.7 | +1.7 |

| Diversified Growth Funds | 7.0 | 9.3 | 6.0 | 7.0 | |

| Property | 10.0 | 9.4 | 10.0 | 8.8 | |

| Infrastructure | 6.0 | 6.0 | 8.0 | 9.0 | |

| Private Equity | 1.0 | 0.5 | 3.0 | 0.8 | |

| Private Debt | 3.0 | 2.0 | 3.0 | 2.9 | |

| Total Alternatives/Other | 27.0 | 27.2 | 30.0 | 28.5 | -1.5 |

Conclusion

It was pleasing to see the good progress the Fund had made in increasing its funding level from 91% to 98% at the 2022 Triennial Valuation, although this has fallen back to some extent as a result of the difficult market conditions over the past year. As a long-term investor, the Fund can take some bumps along the road, so long as the long-term returns remain strong.

The Fund will also continue to manage the ESG impacts of our investments in line with the expectations of fund members as demonstrated by the survey that we undertook during the year. Investing in companies with a sustainable business plan should be supportive of maximising long term investment returns and managing risk.

Peninsula Pensions, the share service that administers pension benefits for both the Devon and Somerset Pension Funds, continues to perform well. It is good to see regular compliments being received from pension fund members about the service they receive.

The Fund remains committed to ensuring that it provides an excellent service to pension fund members and value for money for both pension fund members and local taxpayers.

Angie Sinclair

Director of Finance and Public Value

Summary Pension Fund Accounts

Fund Account

| 2022 £000 | 2023 £000 | |

|---|---|---|

| Contributions and benefits | ||

| Contributions receivable: | ||

| Employers | 128,172 | 141,245 |

| Employees | 45,260 | 49,905 |

| Transfers in from other schemes | 13,324 | 13,253 |

| Total | 186,756 | 204,403 |

| Benefits Payable | ||

| Pensions | (168,391) | (176,799) |

| Lump Sums | (29,018) | (27,720) |

| Death Benefits | (3,623) | (3,826) |

| Refunds | (596) | (982) |

| Transfers out to other schemes | (26,037) | (9,139) |

| Total | (227,665) | (218,466) |

| (40,909) | (14,063) | |

| Management Expenses | (28,453) | (28,635) |

| Return on Investments: | ||

| Investment Income | 33,647 | 39,115 |

| Change in market value of Investments | 380,768 | 95,569 |

| Net Return on Investments | 414,415 | 56,453 |

| Net Increase (Decrease) in the Fund during the year | 345,052 | 99,152 |

| Add: Opening Net Assets of the Fund as at 1 April | 5,066,930 | 5,411,983 |

| Net Assets of the Fund as at 31 March | 5,411,982 | 5,312,831 |

Net Asset Statement

| Investments at Market Value | 2022 £’000 | 2023 £’000 |

|---|---|---|

| Long Term Investments | 838 | 707 |

| Pooled Investments | 4,883,580 | 4,780,960 |

| Pooled Property Investments | 453,953 | 455,507 |

| Forward Currency Contracts | (2,303) | 2,063 |

| Foreign Currency | 13,908 | 1,478 |

| Short Term Deposits and Cash Equivalents | 8,457 | 57,337 |

| Cash and Bank Deposits | 53,680 | 3,550 |

| Investment Payables and Receivables | (10,253) | 0 |

| Total | 5,401,860 | 5,301,602 |

| Long Term and Current Assets | 18,350 | 18,143 |

| Long Term and Current Liabilities | (8,228) | (6,917) |

| Net Assets of the Fund as at 31 March | 5,411,982 | 5,312,831 |

Current Investment Managers

Managers and Mandates

| Market Value 31 March 2023 £’000 | % of Total Investments % | |

|---|---|---|

| Brunel Pension Partnership | ||

| Passive Equities | 1,412,644 | 26.5 |

| Active Global High Alpha Equities | 296,954 | 5.6 |

| Active Global Small Cap Equities | 280,945 | 5.3 |

| Active Emerging Market Equities | 236,625 | 4.5 |

| Active Sustainable Equities | 520,825 | 9.8 |

| Sterling Corporate Bonds | 347,525 | 6.6 |

| Multi-Asset Credit | 634,549 | 12.0 |

| Diversifying Returns Fund | 368,476 | 7.0 |

| Property | 467,941 | 8.8 |

| Infrastructure | 342,171 | 6.5 |

| Private Equity | 45,019 | 0.8 |

| Private Debt | 62,257 | 1.2 |

| DCC Investment Team | ||

| Infrastructure | 134,846 | 2.5 |

| Private Debt | 89,255 | 1.7 |

| Cash | 61,570 | 1.2 |